Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Get Ready To Buy a Home by Improving Your Credit Score

The idea of buying a new home might be on your mind in the next year. It’s an exciting goal to set, and it’s never too early to start laying the groundwork. One crucial step to prepare for homeownership is improving your credit score.

Improving Your Credit Score

Lenders review your credit to assess your ability to make payments on time, pay back debts, and more. It’s also a factor that helps determine your mortgage rate. An article from CNBC explains:

“When it comes to mortgages, a higher credit score can save you thousands of dollars in the long run. This is because your credit score directly impacts your mortgage rate, which determines the amount of interest you’ll pay over the life of the loan.”

This means your credit score may feel even more important to your homebuying plans right now since mortgage rates are a key factor in affordability, especially today.

According to the Federal Reserve Bank of New York, the median credit score in the U.S. for those taking out a mortgage is 770. But that doesn’t mean your credit score has to be perfect. An article from Business Insider explains generally how your FICO score range can make an impact:

“. . . you don’t need a perfect credit score to buy a house. . . . Aiming to get your credit score in the ‘Good’ range (670 to 739) would be a great start towards qualifying for a mortgage. But if you’re wanting to qualify for the lowest rates, try to get your score within the ‘Very Good’ range (740 to 799).”

Working with a trusted lender is the best way to get more information on how your credit score could factor into your home loan and the mortgage rate. As FICO says:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single “cutoff score” used by all lenders and there are many additional factors that lenders may use to determine your actual interest rates.”

If you’re looking for ways to improve your score, Experian highlights some things you may want to focus on:

- Your Payment History: Late payments can have a negative impact by dropping your score. Focus on making payments on time and paying any existing late charges quickly.

- Your Debt Amount (relative to your credit limits): When it comes to your available credit amount, the less you’re using, the better. Focus on keeping this number as low as possible.

- Credit Applications: If you’re looking to buy something, don’t apply for additional credit. When you apply for new credit, it could result in a hard inquiry on your credit that drops your score.

A lender will help guide you through the process from start to finish, from assessing which range your score falls into and telling you more about the specifics for each loan type.

Bottom Line

As you set your sights on buying a home in the upcoming year, focusing on improving your credit score could help you get a better mortgage rate when the time comes. If you want to learn more, connect with a trusted lender.

Resources

More resources for your homeownership journey:

Buying a Home in Spring 2023

There is still a shortage because there are fewer houses for sale than in normal years before the pandemic even though there are more houses for sale now than there were at this time last year. Here’s what Realtor.com has to say about buying a home in Spring 2023 in their Monthly Housing Market Trends Report :

“While the number of homes for sale is increasing, it is still 43.2% lower than it was before the pandemic in 2017 to 2019. This means that there are still fewer homes available to buy on a typical day than there were a few years ago.”

Buying a Home in Spring 2023

The lack of homes on the market right now will affect how you are buying a home this spring. Because there aren’t many homes on the market, buyers who think about what they need and what would be nice will do better in their search.

How do we start? Get pre-approved for a mortgage. Pre-approval helps you figure out how much you can borrow for your home loan, which is important when putting together your list. You don’t want to fall in love with a home that you can’t afford. Once you know your budget well, making a list of all the features you want and need in a home is the best way to figure out their order of importance.

Here’s a great way to start thinking about them:

- Must-Haves: A house won’t work for you and your way of life if it doesn’t have these things.

- Nice-To-Haves: These are things you’d like to have but don’t need. Nice-to-haves aren’t deal-breakers, but if a home has all of the must-haves and a few of these, it’s a strong candidate.

- Dream State: This is a place where you can think big. Again, you don’t need these features, but if you find a home in your price range that has all the must-haves, most of the nice-to-haves, and any of these, it’s a clear winner.

Lastly, once you’ve made your list and put it into groups that make sense to you, talk to your real estate agent about it. They can help you make the list even more specific, give you advice on how to stick to it, and find a home in your area that fits your needs.

Thinking about buying a home this spring? Send us a message and get a copy of our Spring 2023 Home Buying Guide.

Resources

More resources for your homeownership journey:

Pre-Approval in 2023: What You Need To Know

One of the first steps in your home-buying journey is getting pre-approved. To understand why it’s such an important step, you need to understand what pre-approval is and what it does for you. Business Insider explains:

“In a preapproval [sic], the lender tells you which types of loans you may be eligible to take out, how much you may be approved to borrow, and what your rate could be.”

What Is Pre-Approval

Basically, pre-approval gives you critical information about the home-buying process that’ll help you understand your options and what you may be able to borrow.

As part of the pre-approval process, a lender will look at your finances to determine what they’d be willing to loan you. From there, your lender will give you a pre-approval letter to help you understand how much money you can borrow. That can make it easier when you set out to search for homes because you’ll know your overall numbers. And with higher mortgage rates impacting affordability for many buyers today, a solid understanding of your numbers is even more important.

Pre-Approval Helps Show You’re a Serious Buyer

Another added benefit is pre-approval can help a seller feel more confident in your offer because it shows you’re serious about buying their house. A recent article from Forbes notes:

“From the seller’s perspective, a preapproval [sic] letter from a reputable local lender often can make the difference between accepting and rejecting an offer.”

This goes to show, even though you may not face the intense bidding wars you saw if you tried to buy during the pandemic, pre-approval is still an important part of making a solid offer. In fact, Christy Bieber, Personal Finance Writer at The Motley Fool explains it may be the most important part of making an offer:

“Pre-approval maximizes the chances you’ll be able to actually close the deal – and sellers want to see that.

The fact that a pre-approval gives you a better chance of getting your offer accepted is undoubtedly the most important reason to complete this step . . .”

Bottom Line

Getting pre-approved is an important first step toward buying a home. It lets you know what you can borrow and shows sellers you’re serious about purchasing their home. Connect with a local real estate professional and a trusted lender so you have the tools you need to buy a home in today’s market.

Additional Home Buying Resources:

How Much You Need To Save for a Down Payment

If you’re getting ready to buy your first home, you’re likely focused on how much you need to save for a down payment. Don’t let a common misconception about how much you need to save make the process harder than it needs to be. It may surprise you.

How Much You Need To Save for a Down Payment

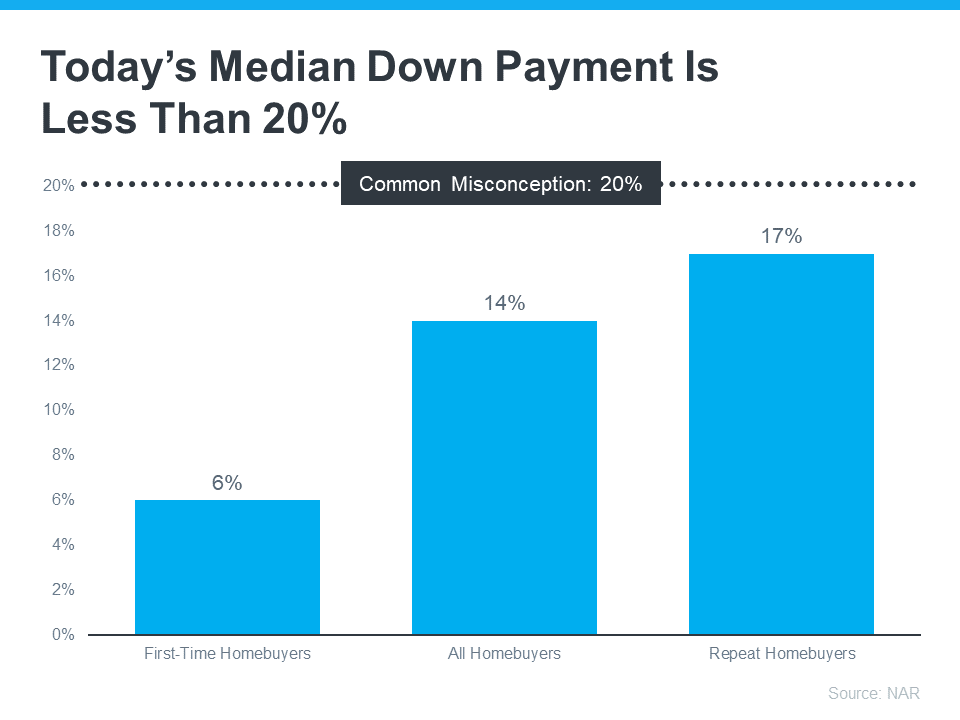

Understand 20% Isn’t Always the Typical Down Payment

Freddie Mac explains:

“. . . nearly a third of prospective homebuyers think they need a down payment of 20% or more to buy a home. This myth remains one of the largest perceived barriers to achieving homeownership.”

Unless specified by your loan type or lender, it’s typically not required to put 20% down. This means you could be closer to your homebuying dream than you realize. According to the National Association of Realtors (NAR), the median down payment hasn’t been over 20% since 2005. In fact, the median down payment today is only 14%. And it’s even lower for first-time homebuyers at just 6% (see graph below):

Options For How Much To Save For Your Down Payment

If saving for a down payment still feels like a challenge, know that there’s help available. A real estate professional and trusted lender can show you options that could help you get closer to your down payment goal. According to latest Homeownership Program Index from Down Payment Resource, there are over 2,000 homebuyer assistance programs in the U.S., and the majority are intended to help with down payments.

Plus there are even loan types, like FHA loans, with down payments as low as 3.5%, as well as options like VA loans and USDA loans with no down payment requirements for qualified applicants.

To understand your options, be sure to do your homework. We can help you learn more about down payment assistance programs that might work for you so you can partner with a trusted lender to learn what you qualify for on your homebuying journey.

Bottom Line

How much do you need to save for a down payment? Remember, a 20% down payment isn’t always required. If you want to purchase a home this year, let’s connect. You’ll also want to make sure you have a trusted lender so you can explore your down payment options.

Resources

More resources for your homeownership journey: